Embark on your journey towards starting, expanding, and flourishing in business with the support of SBA-backed financing. Learn about SBA Loan Programs, 504 Debt Refinancing Programs, and explore commonly asked questions about SBA loans.

In search of resources for your brokerage? Find them here.

As of October 1, 2023, SBA guarantee fees are waived for all SBA loans, up to $1 million. Additional savings are available on loans above $1 million, so you can do even more to make your business shine.

Take the guesswork out of SBA financing with our all-in-one guide. Understand loan types, see insider tips and tricks, learn how to repay loans, and so much more.

Every business is different. Find the best SBA loan structure to fit your specific situation and goals. Stearns Bank's seasoned team is happy to assist you.

SBA 7(a) loans are the most commonly used loan option for business financing. These loans can be used for a wide range of purposes, including business acquisitions, start-ups, working capital, business expansions, debt refinance, equipment and supplies.

Loan terms are dependent upon purpose; for example, while many 7(a) loans are 10 years, the maximum term for real estate loans is 25 years.

General SBA 7(a) loan requirements state that your business must:

Rates are based on the Wall Street Journal prime rate plus a lender spread, which is subject to SBA maximums, based on the term length, or maturity, and the loan size.

While SBA 7(a) is used as a general term, there are many loan types within the program. The best type of loan for your business will depend on how you will use it and when you will need it.

Business owners seeking to buy commercial real estate, equipment, machinery or other major fixed assets can consider SBA 504 loans as an option.

Business owners looking for debt refinance may benefit from the SBA 504 Debt Refinancing Program.

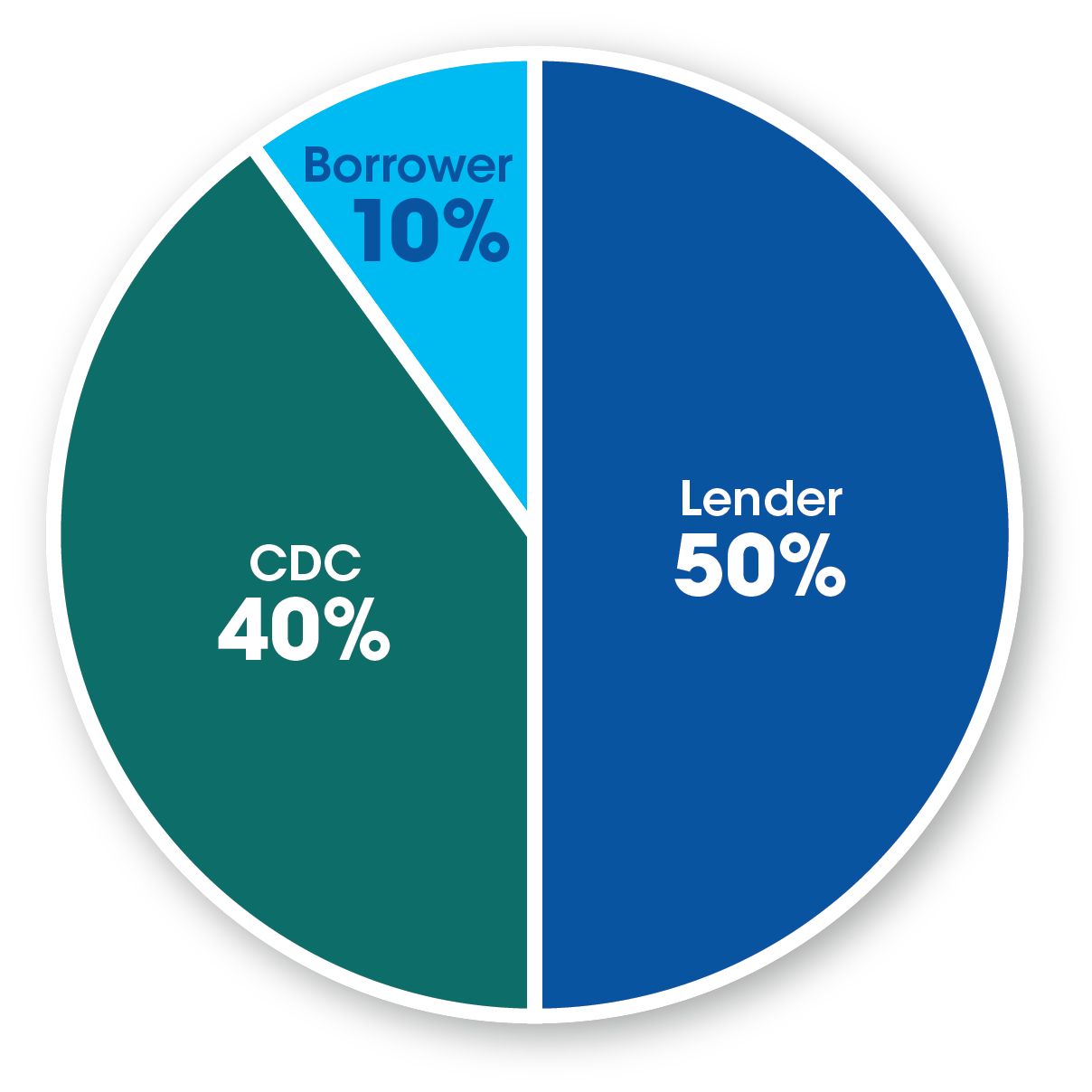

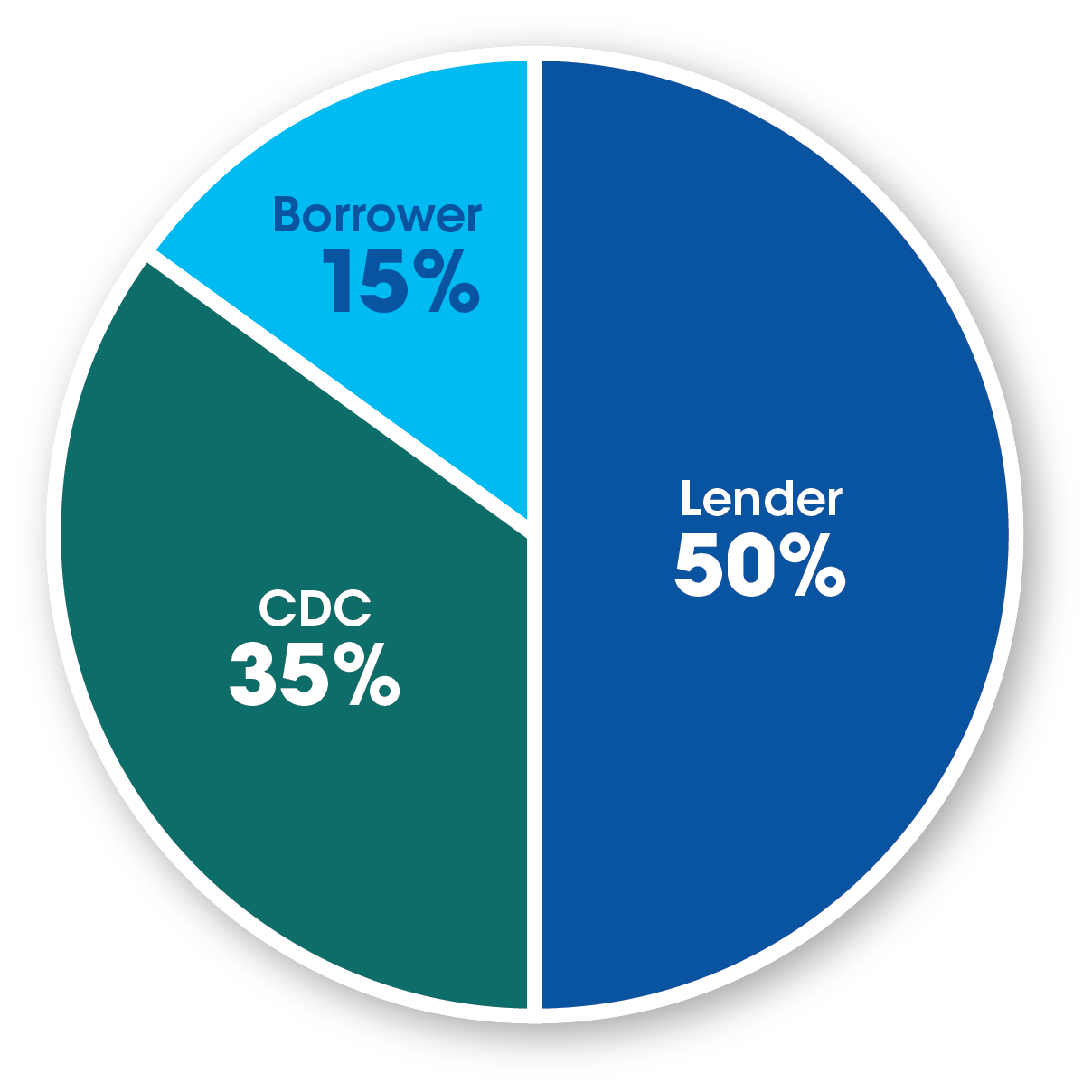

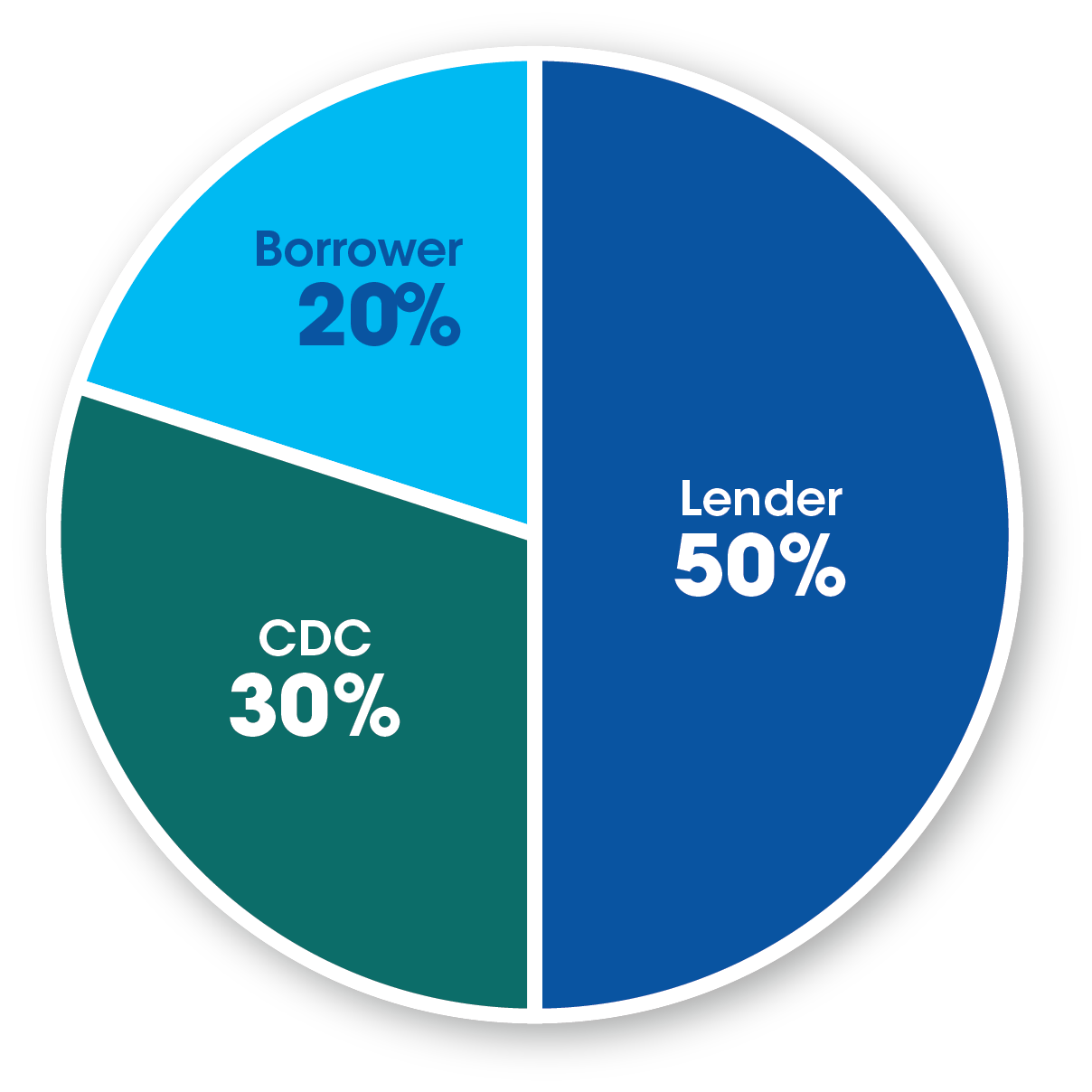

SBA 504 loans differ from other loan programs because of their three-part structure, which includes the lender, a Certified Development Company (CDC) and a borrower.

Varying circumstances affect the model breakdown and down payment responsibility of the borrower within that structure:

| Business Type | Payment Responsibility |

|---|---|

| Typical business in operation for more than two years |  |

| Start-up or new business in operation for less than two years OR Special-purpose property in business for more than two years |  |

| New business AND special purpose property |  |

A special purpose property is one that is not easily converted for other uses and where the operation of the business is tied directly to the real property value and physical location. Examples include car washes, museums, sports arenas, gas stations, hospitals and theatres.

Although the borrower’s contribution is higher in a special purpose property, SBA financing is often a better option than conventional terms, which often require upwards of 30% down from borrowers.

To be eligible for a 504 Loan, your business must:

There are other general eligibility standards for an SBA 504 loan including SBA size guidelines, qualified management expertise, and a feasible business plan. Loans cannot be made to businesses engaged in nonprofit, passive, or speculative activities.

The SBA 504 Debt Refinancing program is for business owners with an existing real estate loan. By refinancing long-term debt, or consolidating multiple loans, the program can help you save money with lower payments and a lower fixed interest rate.

Working with Stearns Bank, a Preferred SBA Lender, you can:

| Lower your interest rate Refinance at a rate below conventional long-term interest rates, saving significant money over the term of your loan |

| Reduce monthly debt payments Lower payments by extending loan terms up to 25 years, easing your debt burden and cash flow challenges |

| Consolidate debt Consolidate high-interest, adjustable-rate debt at a lower, fixed interest rate |

| Obtain cash Borrowers can obtain cash for up to 20% of appraised businesses assets to meet future operating expenses |

| Release equity, reinvest in your business Equity tied up in fixed assets can be turned into cash, which you can reinvest for growth and expansion |

| Save on out-of-pocket expenses – Borrowers can finance ordinary closing costs, rolling them into their new loan |

Stearns Bank is experienced with SBA programs, including SBA 7(a) and SBA 504. You will meet personally with a lender, who will review your current business situation and plans, and develop creative financing options that fit you.

With quick turnaround time, often in a matter of hours, SBA Express loans are a great option to help increase your liquidity.

SBA Express loans can help your business operate or expand when funds are not readily available. These fully amortizing loans have no prepayment penalties and are available to a range of businesses, excluding startups.

Borrowers may use SBA Express loans in a variety of ways, including:

SBA Express loan requirements state that your business must:

From weathering a slow season to exploring a new expansion opportunity, or to catch up on expenses, an SBA Express loan could be the link needed to cross into the next phase of business.

Used to help businesses enter and expand into international markets, the SBA’s International Trade Loan (ITL) offers a combination of fixed asset, working capital financing and debt refinancing.

To be eligible, your business must:

To be eligible to purchase goods or services from your business, foreign buyers must be in countries wherein the Export-Import Bank of the U.S. is not prohibited from providing financial assistance.

For the facilities and equipment portion of the loan, proceeds may be used to acquire, construct, renovate, improve or expand these assets in the U.S. to produce goods or services involved in international trade.

Speed and efficiency are top priority. Decisions are made quickly, with loans up to $5 million approved in just days.

The loan experience is simple and genuinely connected with one point of contact, every step of the way.

For SBA loans involving construction, our internal construction loan management team keeps every detail in check.

Changing budgets and other details are to be expected. We work with you through re-approvals and other updates.

As part of the SBA Preferred Lender Program, we can work faster and more efficiently than non-program lenders.

Access equity by refinancing eligible business expenses with repayment terms up to 25 years. Loans are subject to all applicable loan requirements of the SBA 504 Loan Program.

General qualification criteria:

Always know the status of your loan request with the Stearns Bank Customer Portal. Upload documents and statements required for your application and follow your submission progress.

Reach your business checking and savings goals faster with simple, smart and rewarding BusinessSmart™ accounts. Earn interest and cash back with the convenience of online and mobile banking.

SBA loans often require less borrower equity. SBA loans can greatly benefit small businesses that need capital for a start-up, expansion, inventory, buildings, equipment, exporting and other needs. Terms are typically 7 to 10 years and may be up to 25 years in situations involving real estate.

Stearns Bank understands you’re busy and we’re committed to make your financing a simple process. Loans are approved with speed and precision. Loans greater than $350,000 often are approved in a few days. With Stearns Bank, the application process is fast and simple. Just provide us with basic information about you, your business and your financing needs. We’re ready to fund when you’re ready to close.

You’re in control of the timeline. We have innovative tools available to speed up the process, including document review and sign-off using any device from anywhere you choose. The Stearns Bank Customer Portal provides drag-and-drop secure document submission along with full visibility, any time, to your SBA loan closing. With Stearns Bank, you control the pace to closing and you determine how quickly you want to receive the money.

You name it. All types of business-related costs can be included in your SBA financing request. These costs include: start-up, acquisition, remodel, expansion, succession, real estate purchase, construction, equipment, leasehold improvements, inventory, working capital, franchise fees and debt refinance. Stearns Bank has decades of experience as a Preferred SBA Lender, so just call us and ask.

The SBA loan program allows for a lower equity injection than many other financing options. Stearns Bank will work with you to find the right balance of capital and equity based on your business, your cash flow and growth plans.

If you’re financing the purchase of equipment or real estate with an SBA loan, that equipment or real estate will serve as collateral. Often, SBA loans can be secured without additional collateral outside of the business’s assets. Most small business loans can be extended without being fully secured by collateral. Stearns Bank, as a Preferred SBA Lender, has some discretion as to whether collateral is optional or required on some SBA loans.

Generally, no. Most SBA loans do not have a prepayment penalty, allowing you to manage the principal balance of your loan. SBA loans with a longer term may have a minimal prepayment penalty in the first three years. However, this only applies to loans with principal reductions of 25% or more.

Stearns Bank has developed an efficient process to speed up loan closing. We try to reduce documentation where we can to make things easier on our customers. Typically, you’ll need to provide your business information, organization documents, lease agreement (if leasing space for operations or production), insurance information and a construction quote (if building or expanding). The Stearns Bank Customer Portal provides an easy, safe and secure way to collect all documentation necessary to close the loan. This digital platform provides a detailed list of the documents needed with real-time updates on your loan progress as documents are submitted. With Stearns Bank, you’ll have the same experienced lending team that originated your loan assist throughout the closing process.

Quite simply, call and talk to us! Stearns Bank’s customized application and streamlined loan closing make the process easy. We understand your individual needs and we’re ready to work with you to Get the Job Done!

There are typically fewer fees associated with an SBA loan compared to other conventional loans. This is due to SBA limitations on the amount and type of fees that can be charged to a borrower. With Stearns Bank, all fees are transparent and fully disclosed, so there are no surprises. And, these fees can be included in the financing package.

All fees must be included in the project cost. If money spent prior wasn’t included in the project cost, and now you have the expense, it’s not automatically given as equity credit. Project costs prior to receiving a loan are reviewed on a case-by-case basis.

Yes! Personalized service is our commitment to you. At Stearns Bank, the same loan officer and loan team will work closely with you for the life of the loan. We understand every individual has a communication preference. Therefore, you can easily connect with your loan officer and other Stearns Bank team members by phone, by email or via the chat feature within the Stearns Bank Customer Portal – our digital platform for fast, secure communications and document submission. Additionally, Stearns Bank offers a best-in-class servicing team dedicated to help you for the life of your loan.

Working with a bank that has vast knowledge and experience with SBA loans, like Stearns Bank, is highly beneficial. We believe it’s critical that you understand and are comfortable with each step in your financing, from application to closing and beyond. Not all financial institutions do SBA loans the same way. Our goal is to do things quickly and efficiently. We provide our customers real-time updates with our Customer Portal. With the portal, we try to make our customers' lives a little easier by providing a transparent checklist to show what they have to do to close their loan. Stearns Bank has been providing SBA loans for decades and takes great pride in Getting the Job Done!

Yes. Stearns Bank has been a Preferred SBA Lender for decades. This designation means Stearns Bank has authority to make its own decisions on SBA loans, such as approving and closing, without having to go to the SBA for approvals, closing or funding. As a Preferred SBA Lender, Stearns Bank has been audited and approved by the SBA for the SBA Loan Program, meeting all eligibility criteria. The criterion includes proficiency in processing and servicing SBA-guaranteed loans. This designation allows Stearns Bank to source, approve and fund SBA loans to customers throughout the U.S.

Yes. There is no limit on the number of SBA loans you can have. The SBA Loan Program allows up to $5 million in SBA loans to any one borrower. This makes it easy and convenient to work with Stearns Bank on the initial and any future SBA loans, so we can help your business grow today and well into the future.

Yes. The bank you choose for financing will affect the time it takes to approve and close your loan. There can be considerable differences in the execution, delivery and servicing of an SBA loan. Stearns Bank is a Preferred SBA Lender, highly experienced in all types of SBA lending. We streamline and expedite the SBA application-to-funding process. SBA loans through Stearns Bank save you time and money by making your SBA experience flexible, fast and simple.